When you get married, you start a new chapter inlife. Many new responsibilities come with new relationships. By the time you think to extend your family. And when you have your first child, you probably do not know much about the care of the child. You do each and everything you can do for your child. You take all his/her responsibilities but you also think about his/her financial responsibilities of the future. Many people ignore the financial responsibility topic but it is a serious case. you should take this seriously as by the time expenses get increases. This is also a considerable think for experienced parents as well. They have two or more kids and a huge financial burden. So, they should think about the best they can do to secure their kids’ future.

You should take some important financial measures to secure your family’s future. As a financial advisor, I would suggest some smartest and intelligent financial moves to secure your children’s future. You should read it out full whether you are a new parent or an experienced one.Following are the important financial moves.

1. Build an accidental trust.

The important thing you could do is build an accidental trust as a guardian for your kid. Create a will and mention the guardian name other money-related details in it. By choosing a guardian, you will be ensuring that your kid is receiving the same values you want to give him. And an equal amount of money you have put for your child. I understand as a parent, you put a lot of your effort to save money for your kid. And this trust will ensure you that your kid will receive his money according to your plan. Your kid will get the full money after he will get 18, according to the law.

2. Check out all the beneficiary documents by the time.

This is an important task you have to do to secure your kid’s future. Check your beneficiary documents with the time. Your will is not enough for the beneficiary documents. So, you have to update all the records by the time. So, in the future, your kid will not face any problem for your retirement amount. If you do not update your beneficiary records you may leave a hitch for your kid. He may get suffer a lot after you. So, set all the documents ready and your kid will get the best of it.

3. Buy the best saving plan.

There are many saving options for families now in the country. You should also buy the best saving plan. Save your money when you are earning well. It will help you and your kids out in the future. Also, it is the easiest way to secure your kids’ future. Your saving plan will help your children on their marriage or for higher education. It is up to you which saving plan you will select.

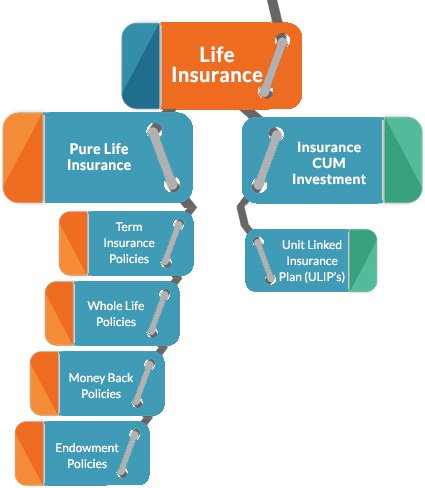

4. Buy life insurance for you and your spouse.

Buy life insurance for yourself and for your wife also. The recovery amount will help your kids after you. If you left your kids orphan, definitely, they will need money to survive. After you, your life insurance money will help them. To be financially strong is the most important thing to live in this world. So, buy life insurance that will secure your children’s future.

5. Buy disability insurance for yourself.

Disability insurance is also important for everyone. If you are doing work with some machines or you are a traveler you may get an accident and get disable at any stage of life. After your disability, your potential to work may get reduced. So, you need a specific portion of your income to survive. Disability insurance will give you that amount. So, buy disability insurance for you.

6. Buy an insurance policy for your kid.

You should buy an insurance policy for your children. At a certain age, they will give your kid the whole policy amount. Your kid’s financial future is secure then.

7. Buy a childcare financial service authority policy.

FSA gives you tax-free childcare insurance. Buy it for your kid.